Sustainability audits are reinforced with the new IAASB manual, International Standard on Sustainability Assurance.

- Art Dam

- Nov 15, 2024

- 2 min read

Global, Friday, 15 November 2024.

Aimed at establishing a new standard for practitioners in carrying out sustainability assurance engagements - i.e. audits - the International Auditing and Assurance Standards Board (IAASB) announced the publication of its finalized International Standard on Sustainability Assurance 5000 (ISSA 5000).

Followed in more than 130 jurisdictions, IAASB is an independent body that serves the public interest by setting high-quality international standards for auditing, quality management, review, other assurance, and related services.

This is a much needed and expected standard, considering times when integrity is frequently put at stake in several occasions, including the growing reporting on sustainability and climate-related risks by companies around the world.

External assurance (audit) plays a key role in enhancing trust and confidence in financial and non-financial reporting.

According to the press release “this standard will serve as a comprehensive, stand-alone standard suitable for any sustainability assurance engagements. It will apply to sustainability information reported across any sustainability topic and prepared under multiple frameworks. The standard is also profession agnostic, supporting its use by both professional accountant and non-accountant assurance practitioners”.

The International Organization of Securities Commissions (IOSCO), the international body of securities regulators, has issued a statement of support for ISSA 5000. Click here to read it.

Click at the image below to read the press release from IAASB and access much more information and references about the ISSA 5000. The good news is that the portal is available in all languages, although the standard is still only in English.

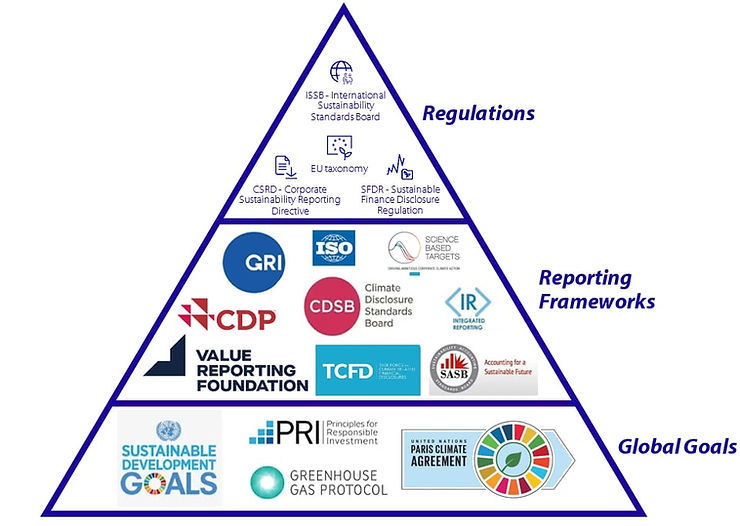

Needless to say that reporting requirements themselves have been also subject to regulatory attention everywhere, specially the IFRS climate and sustainability reporting standards by the International Sustainability Standards Board (ISSB).

You may also like to read these 8 illustrative examples of disclosing climate-related uncertainties in financial statements, IASB public consultation.